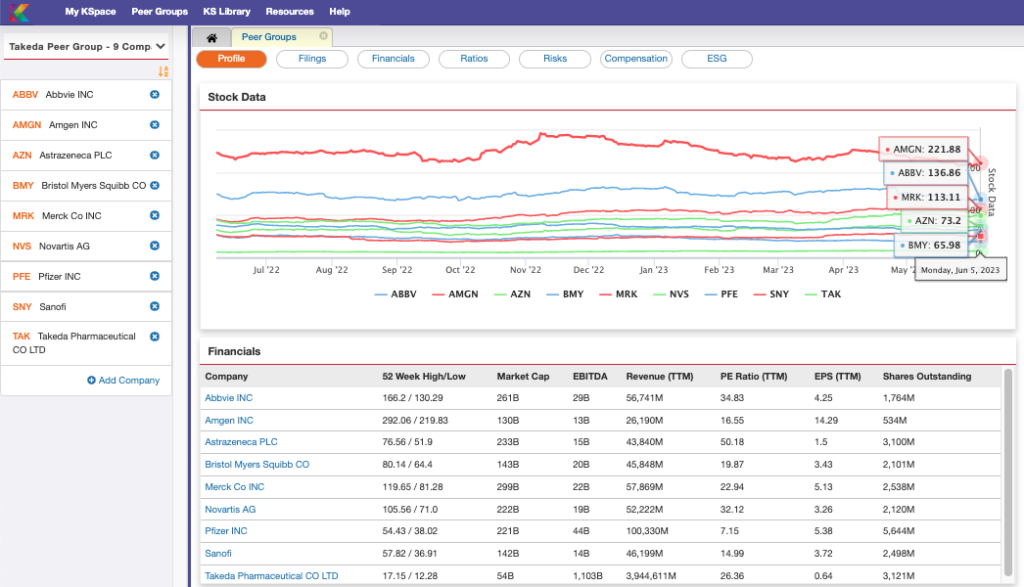

Kaleidoscope helps you continuously monitor investments in company and their securities, investment companies and funds, municipal advisors, or registered investment advisors with real-time alerting on news and corporate activity such as ESG disclosures, quarterly financial results, turnover in executive ranks, workforce layoffs, mergers, acquisition, new financial obligations, new product lines and dozens of other topics. Then add complete stock history charts, immediate access to transcripts and audio of quarterly earnings calls, key performance indicators, and “as reported” fundamental financials, you’ve got a formula for staying informed with actionable intelligence.